Internal audits are not just prep work for external validation. They are a strategic tool that helps organizations uncover blind spots in operations, security, finance, and compliance, before external auditors, regulators, or worse, attackers do.

According to Deloitte, 82% of internal audit functions have increased their impact in the last three years, but only 14% feel they have reached their full potential.

For any company pursuing certifications like SOC 2, ISO 27001, or undergoing financial reporting audits, internal audits are the dry run that ensures you do not fail under pressure.

| TL;DR Internal audits focus on regulatory compliance, governance processes, risk management, operational efficiency, and fraud detection and prevention. Unlike external audits, internal audits are continuous and forward-looking. It includes risk assessments, control testing, risk analysis, reporting, etc. The 5Cs of internal audit are condition, criteria, cause, consequence, and corrective action. |

What is an internal audit?

Internal audit is an independent review that evaluates and improves an organization’s internal processes around risk management, control environment, and governance.

The goal of an internal audit is to proactively evaluate how well your organization’s systems, controls, and workflows are functioning and to spot weaknesses before they spiral into costly issues.

This could mean identifying outdated access policies, unmonitored financial transactions, weak password practices, or underperforming processes that could derail strategic initiatives.

Key focus areas include:

- Governance processes: Whether your leadership structures, decision rights, and oversight mechanisms are functioning as designed.

- Regulatory compliance: If your organization is adhering to laws and standards like SOC 2, ISO 27001, HIPAA, or GDPR, not just in policy, but in daily execution.

- Risk management: How well your company is identifying, tracking, and mitigating risks across operations, IT, finance, and third-party vendors.

- Operational efficiency: Whether internal workflows, systems, and teams are delivering optimal results or wasting time and money due to outdated processes.

- Fraud detection and prevention: Whether internal controls are strong enough to catch irregularities, unauthorized access, or misuse of funds before they escalate.

Internal audits vs external audits

Here are the key differences between internal and external audits:

| Feature | Internal Audit | External Audit |

| Purpose | Improve internal processes and risk management | Provide independent assurance to external stakeholders |

| Performed By | In-house team or outsourced internal auditors | Independent third-party auditors |

| Scope | Broader (operations, compliance, IT, etc.) | Focused on verifying compliance, control effectiveness, and reporting accuracy for stakeholders |

| Frequency | Ongoing/regular | Typically annual |

| Focus | Forward-looking, continuous improvement | Independent evaluation of compliance and internal control accuracy |

Why is an internal audit important?

Internal audits are essential for organizations because they highlight what is working, what needs improvement, and where risks may exist. By uncovering inefficiencies, compliance gaps, and potential threats early, they support better decision-making, enhance operational performance, and build stakeholder confidence.

Here is why you should care about getting an internal audit done:

- Risk reduction: Identify risks across departments, whether operational, financial, or regulatory, and mitigate them before they escalate.

- Operational efficiency: Uncover process gaps, bottlenecks, and inefficiencies that are slowing your business down.

- Fraud detection: Spot irregularities early and implement safeguards to prevent fraud and data breaches.

- Compliance confidence: Keep your company aligned with ever-changing regulations (SOC 2, ISO 27001, GDPR, you name it).

What is the purpose of an internal audit?

Internal audits’ main purpose is to strengthen an organization’s integrity, efficiency, and risk posture. By offering independent insight into how governance, controls, and risk management processes function, audits help ensure the organization stays aligned with its objectives and is better equipped to protect its assets.

Key purposes include:

- Evaluate internal controls: Review how effective your organization’s controls are in mitigating risk.

- Ensure compliance: Confirm that the company is meeting all legal, regulatory, and internal policy requirements.

- Assess risk management: Check if your risk identification and mitigation strategies are robust and proactive.

- Optimize operations: Identify inefficiencies or redundancies and recommend improvements to streamline processes.

- Safeguard assets: Ensure that both digital and physical assets are properly protected.

- Support strategic decisions: Provide executives with trusted insights that guide smarter business decisions.

- Enhance accountability: Keep all departments and stakeholders aligned and accountable for their risk and compliance responsibilities.

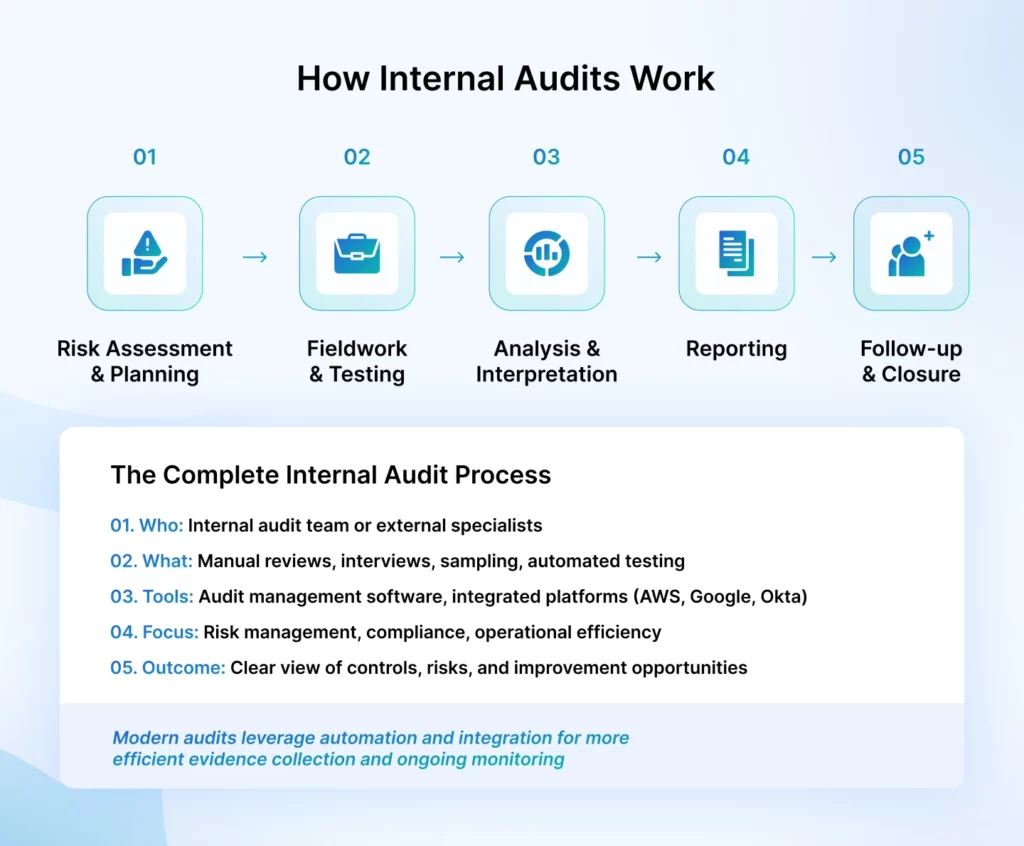

How does an internal audit work? (With template)

Internal audits are typically conducted by an in-house audit team (often led by an Internal Auditor), but they can also be outsourced to specialized internal audit firms for independence or when internal expertise is limited.

A combination of manual reviews, interviews, sampling techniques, and audit management tools are used to carry out the process. Modern organizations are increasingly adopting internal audit software that integrates with systems like AWS, Google Workspace, Okta, and financial platforms to automate evidence collection, control testing, and reporting.

Download ISO 27001 Internal Audit Template

Here’s a detailed look at every phase of an internal audit.

1. Risk assessment & audit planning

The internal audit process always starts with a risk assessment, which forms the basis of your audit plan. This is where the audit team defines the audit universe – all the business units, systems, processes, or departments that could be audited, and ranks them by their risk profile.

High-risk areas, like IT security, access control, finance, or third-party vendor management, are prioritized. The goal is to identify where the organization is most exposed and where internal controls are most critical.

From here, the audit plan is developed. This includes defining audit objectives (e.g., evaluating access control for SOC 2, or financial process validation for SOX), outlining the scope, determining what frameworks or policies apply, and assigning resources.

This phase typically concludes with a formal kickoff meeting involving key stakeholders, where timelines, responsibilities, and expected deliverables are communicated. There are usually checkpoints scheduled during the audit to ensure alignment, progress tracking, and transparency.

2. Fieldwork & testing

Fieldwork typically starts with document reviews: auditors examine policies, access logs, change records, asset inventories, incident reports, and control matrices to understand how systems are supposed to work. They perform walkthroughs, following a process or transaction from beginning to end (e.g., from employee onboarding to access provisioning to offboarding) to verify actual practice.

But it does not stop there. Auditors conduct employee interviews to uncover how processes are implemented in practice versus how they are written on paper. This helps identify whether staff are trained, policies are clear, and controls are realistic.

Most importantly, auditors perform sampling and control testing. For example, they may test whether all terminated employees in the past 3 months had access revoked within the required timeframe, or whether monthly reconciliations were properly approved.

This phase also includes on-site observations, process inspections, and in some cases, penetration testing or vulnerability assessments (for IT-focused audits).

3. Analysis and risk interpretation

Once the evidence is gathered, the audit team moves into the analysis phase, where raw findings are converted into actionable insights.

First, auditors benchmark actual practices against the defined criteria: internal policies, external regulations (like ISO 27001 or SOC 2), and best practices. They identify control failures, inconsistencies, and process breakdowns.

Then comes root cause analysis – the critical thinking piece of the audit. Auditors ask: Why did this happen? Is this an isolated incident or a systemic issue? Was the cause technical (e.g., a failed automation), procedural (e.g., outdated policy), or cultural (e.g., lack of accountability)?

4. Reporting

The audit report is structured to give leadership a strategic overview of findings, followed by actionable, department-specific guidance. It typically includes:

- Executive summary: High-risk issues, their root causes, and potential business impact.

- Detailed findings: A breakdown of each control failure or issue, with evidence, responsible teams, and regulatory references.

- Risk scoring: Each finding is tagged as high, medium, or low risk, often with impact/probability scoring.

- Recommendations: Specific, prioritized corrective actions – with timelines, suggested owners, and implementation steps.

- Management responses: Each department or control owner provides initial feedback, confirms ownership, or disputes findings (if needed).

5. Follow-up & audit closure

Follow-up is what separates good audits from paperwork exercises. At this stage, the audit team works with department owners to track the implementation of corrective actions.

This could involve:

- Reviewing new or revised policies

- Retesting controls after remediation

- Verifying that employee training has occurred

- Confirming that automated tools or access management fixes have been deployed

In many organizations, this follow-up process is automated through governance and compliance tools that monitor ongoing control performance and flag if an issue re-emerges.

Automated tools (like Sprinto) can take over to ensure controls remain effective over time.

From findings to action plan, automate end-to-end

8 types of internal audits

Internal audits are not one-size-fits-all. Different types focus on different objectives and areas of the business. Let’s understand the eight main types of internal audits:

1. Compliance audits

Compliance audits assess whether your business is adhering to regulatory requirements, legal obligations, and internal policies. They evaluate the effectiveness of your compliance processes, identify gaps in enforcement, and flag outdated or missing documentation.

2. Penetration audits

Penetration audits simulate real-world cyberattacks to identify security vulnerabilities in your infrastructure. These audits go beyond configuration checks to actively exploit weaknesses in systems, networks, and applications.

The goal is to reveal how an attacker could gain access, move laterally, and compromise data or systems. Pen tests are resource-intensive but critical for businesses handling sensitive data or operating in high-risk environments.

3. Risk assessment audits

Risk assessment audits focus on identifying potential threats before they materialize. They involve mapping out risks across departments, scoring them based on likelihood and impact, and evaluating whether existing controls are adequate.

These audits help prioritize remediation efforts and ensure that risk mitigation strategies are proportionate to the exposure. Their effectiveness depends on accurate input and unbiased analysis.

4. IT audits

IT audits evaluate your organization’s technology infrastructure, security practices, data policies, and access controls. They assess whether systems are secure, compliant, and capable of supporting business operations without unnecessary risk.

The audit covers areas such as system architecture, role-based access, encryption protocols, incident response readiness, and disaster recovery procedures.

5. Investigative audits

Investigative audits are initiated in response to suspected fraud, data manipulation, policy violations, or financial misconduct.

These audits aim to uncover facts by reviewing logs, transactions, communications, and user activity. The focus is on accountability – identifying who did what, when, and whether internal controls failed or were bypassed.

6. Performance audits

Performance audits examine whether resources – budget, staff, systems – are being used efficiently and delivering intended results. They assess if business processes are optimized and aligned with organizational goals.

These audits are often used to validate the effectiveness of strategic initiatives, cost reduction efforts, or technology investments.

7. Integrated audits

Integrated audits combine multiple audit scopes – such as IT, compliance, finance, and operations into a single review. They are useful for evaluating interdependent controls and overlapping risk areas.

For example, assessing whether your access control policies meet both cybersecurity standards and compliance requirements. These audits provide a broader view of risk exposure and control effectiveness.

8. Environmental audits

Environmental audits assess how your organization manages its environmental responsibilities. This includes reviewing waste disposal, emissions, energy consumption, hazardous material handling, and supply chain sustainability practices.

These audits help ensure compliance with environmental laws and internal sustainability goals, especially for companies subject to ESG scrutiny.

What are the 5C’s of an internal audit?

The 5Cs of internal audit are a structured reporting framework used by internal auditors to clearly communicate not just what went wrong but also why it happened, what it means, and how to fix it.

Let us break down each “C” and what it should deliver.

1. Condition

The Condition describes the specific issue that was observed during the audit. It should be factual, detailed, and tied to evidence, not vague generalizations.

For example, do not say “Access controls are weak.” Say, “In 3 out of 10 sampled instances, terminated users retained access to critical financial systems for more than 7 days post-termination.”

2. Criteria

The Criteria explains the standard the organization was expected to meet, what should have happened. This could be an internal policy, an external regulation (like SOC 2, ISO 27001, SOX), a service-level agreement, or even a best practice that has been formally adopted.

3. Cause

The Cause identifies why the issue happened. This is often the most overlooked section in internal audit reports and the one executives care most about. A meaningful cause analysis digs deeper than symptoms and focuses on root causes.

Was it a failed automation? A lack of training? A policy that exists but no one enforces? Or maybe an overworked team manually managing processes that should be automated?

4. Consequence

The Consequence outlines the risk or impact associated with the condition. This is where you answer the question: “So what?” A great consequence section goes beyond general terms like “security risk” and ties the finding to real-world impacts like data loss, financial exposure, regulatory fines, reputational damage, or even operational downtime.

5. Corrective Action

The Corrective Action defines how the issue will be addressed – who owns the fix, what steps will be taken, and by when. It should include both short-term remediation (e.g., disabling access for terminated users) and long-term prevention (e.g., automating the de-provisioning workflow and tightening policy enforcement).

Managing internal audits with Sprinto

For many small businesses, startups, and mid-market companies, internal audits still live in spreadsheets, shared drives, and inboxes. What starts as a structured process quickly becomes a reactive scramble, chasing down evidence, aligning stakeholders, and updating last year’s audit checklists that no longer reflect current risks.

But here is the truth: strong audit management is not about doing more work; it is about doing smarter work. That means building a system that is:

- Proactive, not reactive

- Integrated into your risk and compliance programs

- Repeatable and scalable as your business grows

Case in point: When CertPro CPA LLC, a leading audit firm, partnered with Sprinto to conduct audits across multiple businesses, the impact was immediate and measurable. Using Sprinto’s integrated audit environment, they were able to:

- Cut audit time by 90%

- Access real-time audit trails without having to request additional documentation

- Significantly reduce back-and-forth communication with clients

Get a wingman for all your audits

Frequently asked questions

1. What is internal auditing management software, and how does it improve compliance?

Internal audit management software standardizes the audit lifecycle from planning and risk assessment to execution and reporting. It improves compliance by automating routine tasks, reducing manual errors, and ensuring that controls are consistently monitored and tested. These platforms typically come with built-in frameworks, automated reminders, and audit trails, making it easier to demonstrate compliance during external reviews or certification processes.

2. How does internal audit management software handle documentation and evidence collection?

Internal audit software centralizes all audit-related data in a single, secure platform. Evidence—such as logs, screenshots, policy documents, and access reports—can be linked directly to the control or process being audited. This ensures that everything is organized, version-controlled, and available on demand.

3. What is the role of management in internal audit?

Management plays a critical dual role in internal audit, as both a subject and a driver. On one hand, audit teams evaluate how well management is handling risk, governance, and compliance obligations. On the other hand, management is responsible for facilitating the audit process, ensuring transparency, and—most importantly—acting on audit findings.

4. How often should internal audits be performed?

There is no universal rule, but audit frequency should be based on your organization’s risk profile and regulatory obligations. For high-risk areas (like data security or financial reporting), quarterly audits are often best practice. For lower-risk functions, semi-annual or annual audits may suffice. Frameworks like ISO 27001 and SOC 2 typically require at least one formal internal audit per year.

Pansy

Pansy is an ISC2 Certified in Cybersecurity content marketer with a background in Computer Science engineering. Lately, she has been exploring the world of marketing through the lens of GRC (Governance, risk & compliance) with Sprinto. When she’s not working, she’s either deeply engrossed in political fiction or honing her culinary skills. You may also find her sunbathing on a beach or hiking through a dense forest.

Go beyond the surface and uncover the governance, risk, and compliance insights that actually matter.

Win digital goodies for boardroom success

Explore more

research & insights curated to help you earn a seat at the table.