Risk-Based Internal Audit: How to Prioritize, Plan and Mitigate Risks

Your company’s sensitive information is plastered across the internet. You seemed to be locked out of your system, and the ransom to get your access back is hefty, to say the least. You’re scrambling to understand what has happened, and the alarm goes off. Don’t worry; it’s a nightmare that I painted for you, at least for now……

But with cyber threats on the rise, these scenarios have become all too plausible. Hence internal audits have become an essential part of keeping these threats at bay.

An internal audit is a systematic approach that identifies and analyzes these threats and takes proactive measures to mitigate them. It ensures that your organization remains secure, compliant and operationally efficient. And most of all, it makes sure that these nightmares remain a pipedream for hackers.

A risk-based internal audit isolates and focuses on areas that pose the greatest risk. Rather than auditing every function, this approach ensures that resources are allotted where they are needed the most.

Risk-Based Internal Audit: Risk based internal audit is an audit approach that prioritizes and evaluates areas of highest risk within an organization, aligning audit focus with business objectives and risk appetite.

Purpose:

• Identify, assess, and mitigate high priority risks

• Align internal audit efforts with strategic goals

• Improve operational efficiency and compliance

• Enhance visibility into risk and control gaps

6-Step RBIA Process:

1. Define audit objectives (e.g., vendor onboarding, compliance readiness)

2. Conduct risk assessments (evaluate financial, operational, compliance, third-party, cyber risks)

3. Develop audit procedures (scope, depth, testing, reporting)

4. Allocate staff and resources (CAE, managers, SMEs)

5. Report findings and recommend corrective actions

6. Review and iterate continuously with risk monitoring tools

Approaches and Techniques:

• CSA – Involve process owners in control evaluation

• Historical Data – Spot patterns from past incidents

• Risk Appetite – Align audits with acceptable risk levels

• Probability Model – Quantify risk with numerical scores

• Integrated Auditing – Examine cross-functional risk exposure

Benefits:

• Smarter resource allocation

• Focused mitigation plans

• Continuous visibility into evolving risks

• Better ROI than traditional checklist audits

Why Sprinto?

Sprinto brings automation, live dashboards, and integrated GRC capabilities that help you monitor, prioritize, and mitigate risk without manual overload.

What is a risk-based internal audit?

A risk-based internal audit is a systematic approach that identifies, evaluates, assesses, and prioritizes risks that could potentially impact the organization. It finds weak spots before they become threats, takes stock of current responsive measures, and aligns them with business goals.

RBIA (risk based internal audit) is designed to align the internal audit function with the enterprise’s risk management strategy. This audit assures the board of directors and senior management that the risk management process is working effectively and is aligned with business priorities.

According to Lead Auditor at Sprinto, Varenya Penna:

“By focusing on a risk-based approach for internal audits, you not only mitigate threats but also ensure that the audit procedures are aligned with the strategic objectives of the business, allowing you to create a resilient environment”

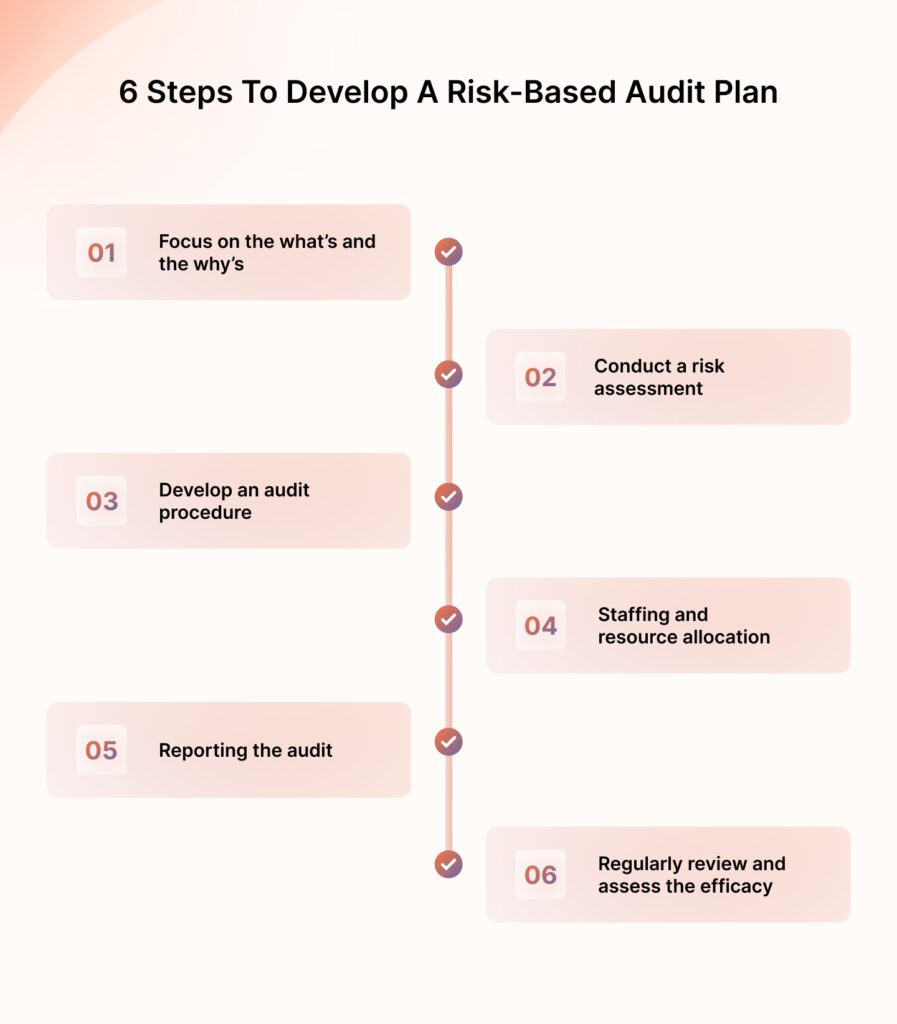

6 Steps to develop a risk-based internal audit plan?

The risk-based audit plan process involves six key steps, namely—understanding the objective, conducting an audit, conducting a risk assessment, and regularly reviewing the process.

A risk-based audit approach enables internal auditors to address organizational risks more in time and deliver timely insights to management to help resolve issues on an ongoing basis.

Here’s how:

Step 1: Focus on the what’s and the why’s

Clearly understand the objective for which you want to conduct the audit. Here are a few reasons organizations generally do a risk based internal audit;

- New vendor onboarding: There are risks associated with onboarding a new vendor and carrying out an audit will ensure that appropriate controls are in place to manage risks. It also speaks to the effectiveness of the due diligence process of your vendor selection.

- Precursor to compliance: To assess the readiness of your organization to implement the compliance program or the legal requirements, RBIA is done. It evaluates your existing controls and identifies any potential gaps that are in need of remediation.

- Mergers and acquisitions: A risk-based internal audit can flag and tackle the risks associated with a potential merger, such as operational, legal, financial, and regulatory.

- Post-incident review: Companies also conduct an internal audit after an incident like a data breach, fraud, or disruption. This is necessary to assess the root cause of the incident and take precautionary measures going forward.

- Operational efficiency: An internal audit can also streamline operational processes in business functions. The objective could be to identify bottlenecks, evaluate the current effective controls in place, or assess the efficacy of the audit activities.

By understanding what your organization’s needs are and aligning them with the goals, you ensure that there is a solid foundation. This is necessary to ensure an effective allocation of resources and to deliver valuable insights through the audit process.

Step 2: Conduct a risk assessment

Conduct a risk assessment through risk identification exercise across all departments. Here are some possible business risk categories for you to consider:

- Financial risks

- Defaulting on loans or other financial obligations.

- Changes in liquidity rates, interest rates, exchange rates, and other economic factors contributing to a higher payback than anticipated.

- Inability to meet any short-term financial demands, i.e. liquidity.

- Insufficient capital.

- Declining profitability or frequent loss-incurring incidents.

- Operational risks

- Mistakes in data processing or, naturally, some human error due to manual operations.

- System failures like IT problems or malfunctions.

- Fraud or misconduct by employees.

- Disaster or outages leading to the inability to keep up with supply chain demand.

- Third party risks

- Breach of terms and conditions by third-party vendors.

- Unreliable third-party service.

- Data mishandling by third parties.

- Compliance risks

- Violations of privacy laws like GDPR, CCPA, et cetera.

- IP infringements.

- Inaccurate financial reporting.

- Failure to comply with compliance regulations leading to a breach or a threat.

- Strategic risks

- Disruptive technologies.

- Negative PR or brand damage due to foreseen or unforeseen circumstances.

- Risks due to mergers or acquisitions.

- Cybersecurity risks

- Data breaches, malware attacks, infectious systems.

- Phishing attacks.

- DDos attacks.

These are potential risks that any and all organizations face. There could be other risks that are specific to your organization, make sure to account for them. Once you have identified these risks, they usually follow a process to assess their likelihood, impact and score. It looks like this:

- Determining the probability of each threat.

- Estimating the potential impact of the said risk.

- Calculating the risk score which is = Likelihood x Impact

- Based on the score, categorize them. High, medium, and low.

High-priority risks: They should be tagged RED and usually risks with severe damage. Financial risks (think 2008 market crash or the COVID-19 pandemic effect), data breaches, regulatory violation breach, and or prolonged system outages are considered high priority risks. These risks might not have a high frequency but the damages caused are deep enough for you to bump them to the reg tag,

Medium-priority risks: They should be tagged YELLOW since their impact is moderate and businesses can bounce back from them. Operational risks, third-party contract breaches, and small market fluctuations are considered medium-priority risks.

Low-priority risks: These can be tagged GREEN and they have minimal impact on the business. Minor data processing errors or small environmental risks are categorized as low-priority risks.

Some of these risks can be managed and mitigated by automating workflows, but understanding the risk landscape can still be a time-consuming process. This is where Governance, Risk, and Compliance come into play. GRC platforms offer solutions that automate processes like risk assessment and management. They give you a clearer picture of the risks and effective ways to mitigate them.

Sprinto is a leading GRC platform that solves this for you. It offers you an integrated risk management system with heat maps that help visualize risks (just like we have above). The heat map gives you a holistic view of the risks and the areas that it will impact. Sprinto also gives you finer details of the data around each risk. It covers the controls, treatment plans, the current status, the progress and the description of each risk.

Check out our video on integrated risk management to learn more

How Sprinto enables integrated risk management?

Breeze through your risk-based audits

Step 3: Develop an audit procedure

Once you recognize the areas that demand the most of your attention, create a detailed program. Here’s what needs to be included in the procedure:

- The scope of each audit

- Outline the areas you would want to focus based on the risks that you identified.

- What is the depth for each audit?

- What do you want to cover and how do you want it covered? Answer the why’s if you can.

- Create a procedure that needs to be followed.

- Select the appropriate sampling and testing techniques that you would want to follow,

- Take note of any data analysis tools you might use.

- Set a realistic timeline and account for the complexity of each audit.

- First you have the pre-audit phase. You gather information, set up meetings, and involve key stakeholders. This usually takes about 2 weeks.

- Once you have your findings, plan your audit and have an audit program in place. This should not take more than a week but give your team some buffer.

- Conduct tests and gather all the evidence that you or your team can. This is an intensive process and can take anywhere from 4 to 8 weeks.

- Audit the findings and draft up a review for the board. While it seems like a simple task, writing up recommendations and focusing on the fixes can take up to 3 weeks.

- Submit your audit and finalize a plan of action to work on the recommendations. Should not take longer than a week.

- Once your plan is ready to be set in motion, start assigning members, heads, auditors and their roles. Allocate budgets for each audit and identify any tools you might need.

- Have a clear communication line, with meetings and escalation trackers in place.

Document the entire procedure for future reference to highlight any trends. Conduct post-audit evaluations to understand the lessons learned.

Make your RBIA plan repeatable. Use this playbook to standardize scope, sampling, and evidence before your next audit.

You could face some blockers along the way, but here are some tips to mitigate them:

- If you face resource constraints, prioritize only high-risk areas. Once you have enough budget and resources, move on to lower-risk areas.

- If you are facing technical complexity, it is best to engage SMEs if you can and allow extra time to better understand the issue.

- If you find yourself with an inadequate audit, trace every step back. Look at everything you documented to gain a better understanding.

Step 4: Staffing and resource allocation

After you have developed the audit procedure, it’s time to assemble your A team and delegate responsibilities. Here’s how to get started:

- Appoint a Chief Audit Executive, or CAE. This person should oversee the entire audit and communicate the findings to the team. They should be well-versed with the process and have the ability to command the team.

- An audit manager should supervise the teams with a more hands-on approach. They should also be able to assess the quality of the work that’s being done.

- Appoint staff and an IT auditor to help you with the documentation and technical expertise respectively.

If you find yourself unable to assemble the team, here are some possible routes you can take:

- Find an external auditor to help you through the audit gaps.

- Upskill your existing team members by conducting training sessions.

- Implement GRC software to automate tasks.

Step 5: Reporting the audit

Once the audit is prepared, your internal audit team needs to analyze the findings. This involves compiling tons of data from various sources.

Your audit should cover the following areas:

- Summary

- Audit objectives and scope

- Findings

- Recommendations

- Plan of action

This is a time consuming, not to mention an error prone, task when done manually.

You can use Sprinto’s risk management module to get a better understanding of things at a glance. Sprinto provides real time data, visualizes risks and also calculates risk scores based on the predefined criteria. The system also tracks treatments and provides a detailed breakdown of the risk. Basically it does all the grunt work for you so that you can present insights to management and have the data ready on hand.

Step 6: Regularly review and assess the efficacy

The effectiveness of the recommendations should be regularly reviewed and assessed. This is crucial so that your methods stay relevant and effective and your organization’s risk profile remains solid. However, doing this manually can lead to oversight as the process is challenging.

You can use continuous compliance tools to address this issue. Continuous compliance tools provide real-time statistics, instead of periodic assessments. This allows for immediate detection and response to new risks and compliance issues.

Continuous compliance platforms not only monitor risks on a regular basis, they also automate the scheduling of more comprehensive and in depth audits. These tools can also integrate with your existing system, gathering data from various sources to give you an accurate view of your compliance and risk status.

Automate risk-based compliance effortlessly

Benefits of a risk-based internal audit

A risk-based internal audit builds a culture of adaptive resilience by anticipating and developing an incident response plan. It mitigates the risks your organization is currently facing and builds a foundation for sustained agility.

Here are 3 other benefits RBIA offers:

1. Comprehensive coverage

RBIA is a comprehensive approach as it covers many parameters, such as previous reports, industry trends, and environmental factors. You can get a bird’s-eye view of your organization’s risk profile, which builds confidence and assurance for the board and senior management.

2. Efficient use of resources

RBIA focuses on high areas and audits them more frequently, as opposed to the low risk ones. Instead of scrutinizing every risk factor, regardless of their risk, this approach ensures that your team focuses on the areas that are more critical. This ensures that risks receive the coverage and attention they deserve and also prevents the team from burning out.

It maximizes your return on investment!

3. Effective risk monitoring

Risk based auditing ensures that there is continuous monitoring of the risks. In the longer run it also equips the team with the ability to identify risks that are still in its early stages. This approach also ensures that your team does not face battle fatigue or is overwhelmed by evaluating each risk thoroughly.

To maximize the efficacy of your audit, design an RBIA that uses techniques tailored to your goals and objectives.

Effortless, Efficient Risk Evaluation

Types of risk-based internal audit approaches and techniques

Each methodology is unique in its approach. While historical data analysis and probability approaches provide data-driven insights through trends, CSA and integrated audit approaches leverage cross-functional collaboration. Understanding these nuances between approaches can help you tailor your auditing approach to best suit your priorities.

Here are 5 risk based audit approaches and techniques that you can leverage to maximize the effectiveness of the audit.

1. Control Self Assessment or CSA approach

CSA or Control Self Assessment is an approach that leverages the expertise of process owners and operational managers. Instead of solely relying on external auditors, CSA involves the experts to evaluate the effectiveness of the controls within their respective areas.

By actively participating in the process, the process owners and operational managers get a better understanding of the risks that are specific to their daily operations and the controls designed to mitigate them.

This approach also fosters a sense of accountability and responsibility within the process owners and operational managers.

2. Historical data analysis approach

Data analytics is a great approach for an RBIA. By looking at historical data, such as security access, incident reports, system activity logs, and other relevant data points, organizations can recognize a pattern and tailor their controls and strategies accordingly.

You can even predict potential breaches based on historical trends, identify the source of incidents, and potentially weed out compromised accounts. This approach should be considered at every step of the audit process.

3. Risk appetite approach

The risk appetite approach focuses on aligning your company’s risk tolerance with its goals. The underlying question to this approach is basically – How much risk is the org willing to take in order to meet the strategic goals?

This approach begins by establishing the level of risk your organization is willing to take. Factors like financial stability, regulations, and other business goals. Once you’ve realized your risk appetite, you can identify areas that pose risks across various functions and departments.

The risk is assessed based on the frequency, intensity, and the likelihood of its occurrence. Controls are then put in place to mitigate said risks. The risk assessment defines how stringent the control process would be.

This is not a static approach. You need to continuously monitor and manage the approach based on the changes in business environment and or laws and regulations.

4. Probability approach

This approach focuses on quantifying risk through elimination. It estimates the likelihood of a threat and its potential impact. Historical data analysis is used to determine the probability of the risk materializing. The probability is based on the frequency of the attack, vulnerabilities in the system, etc., and is assigned a numerical value.

The impact is also assigned a numerical value to allow for objective decision-making. The risk is then calculated by multiplying the likelihood and the impact. .

This approach allows for maximum return on security investment by carefully monitoring and mitigating the risks with the highest numerical value.

5. Integrated auditing approach

This approach examines an organization’ financial documents, internal controls and how they integrate with various departments like IT, HR, legal, operations, and compliance. It takes a granular approach to see how various aspects of an organization interact with each other.

Integrated auditing can unmask risks that arise from an interplay between different functions. For example, some weak link in IT security or controls could leave the financial data of the firm vulnerable, which could be overlooked in a siloed financial audit.

However, it is imperative that you understand the complexity of this approach, as correlation is not always causation.

Ultimately, the aim of risk-based auditing is to provide valuable information that can drive improvements in companies’ practices. It is always advisable that the plan you undertake aligns with your organizational goals and business strategy.

RBIA – an investment

The “it won’t happen to us” fallacy often stems from lack of visibility, undetected data breaches, and/or underestimation of the indirect costs. For many small businesses, one successful attack can be terminal. Even if they’re able to rebuild, the reputation and brand image cannot be repaired for a very long time.

Risk assessments and audit plans are investments whose costs pale in comparison to the costs of cyber breaches. The global average data breach cost was $4.45 million USD, back in 2023.

The question then remains, would you rather afford a risk and compliance management platform or pay for breaches and scams as they show up on your doorstep?

Book a call with our experts to know more.

Frequently asked questions

What is the difference between traditional audit and risk based audit?

The difference between a traditional audit and a risk based audit is primarily on the scope and focus. A risk based audit prioritizes areas with a higher risk score, whereas a traditional audit examines all areas and functions equally. A traditional audit follows a standard checklist approach could and hence prove to be less efficient. But a risk based approach is based on the risk it has assessed and could be more efficient as it allocates resources to areas of greatest concern.

What are the 4 types of risks?

Risks can broadly be categorized into financial risks, operational risks, strategic risks, and compliance risks. Organizations usually implement enterprise risk management frameworks to assess, and manage these risks.

How do you mitigate risk in internal audit?

While an audit does not mitigate risks, it gives you visibility of potential risks. Before they can become threats, an internal audit helps you assess those risks and come up with controls and recommendations to mitigate them. You need a detailed internal audit program to look for finer details and address every risk.

What are audit risk examples?

Audit risk examples include inherent risks, control risks, and detection risks. Inherent risks are pre existing risks that occur due to the nature of the business. These cannot be controlled by audits or the management. Control risks are risks that could occur but not be prevented, detected, or corrected by an organization’s internal control system. They are assessed by auditors, and they can be assessed through an improved and effective control system.

The last one, detection risks are risks that are missed due to inappropriate testing methods, insufficient sampling, or even through misinterpretation of the audit evidence.

Comprehensive Risk Monitoring & Mitigation

Author

Heer Chheda

Heer is a content marketer at Sprinto. With a degree in Media, she has a knack for crafting words that drive results. When she’s not breaking down complex cyber topics, you can find her swimming or relaxing by cooking a meal. A fan of geopolitics, she’s always ready for a debate.Go beyond the surface and uncover the governance, risk, and compliance insights that actually matter.

Win digital goodies for boardroom success

Explore more

research & insights curated to help you earn a seat at the table.