What happens when the global finance systems fail unexpectedly?

In February 2022, a cyberattack on ION Group, a key service provider for banks and brokers, brought down trading systems in Europe and the United States. Overnight, firms were forced to manually process trades, scrambling to stay up with market movements. The disruption lasted many days, revealing a harsh reality: financial institutions are prone to operational collapse.

This is exactly what the EU wants to fix with DORA (Digital Operational Resilience Act).

TL;DR

| Financial institutions and ICT service providers must classify, log, and report every ICT-related incident using a standardized oversight framework to ensure transparency and regulatory compliance. |

| Operational resilience testing—including penetration testing and threat simulations—must demonstrate that financial institutions, including payment institutions, can withstand cyber threats and disruptions. |

| Organizations are responsible for ICT third-party risk, meaning vendors and service providers must meet strict resilience and security standards to prevent supply chain vulnerabilities. |

What is DORA compliance?

The Digital Operational Resilience Act (DORA) is an EU regulation designed to ensure that financial institutions can withstand, respond to, and recover from cyber threats and operational disruptions. It goes beyond traditional IT security by making digital resilience a legal requirement.

DORA applies to banks, insurance companies, investment firms, and a wide range of financial entities, along with their critical third-party service providers, such as cloud platforms and software vendors. It introduces strict rules around risk management, incident report, and digital resilience, which form the pillars of this regulation.

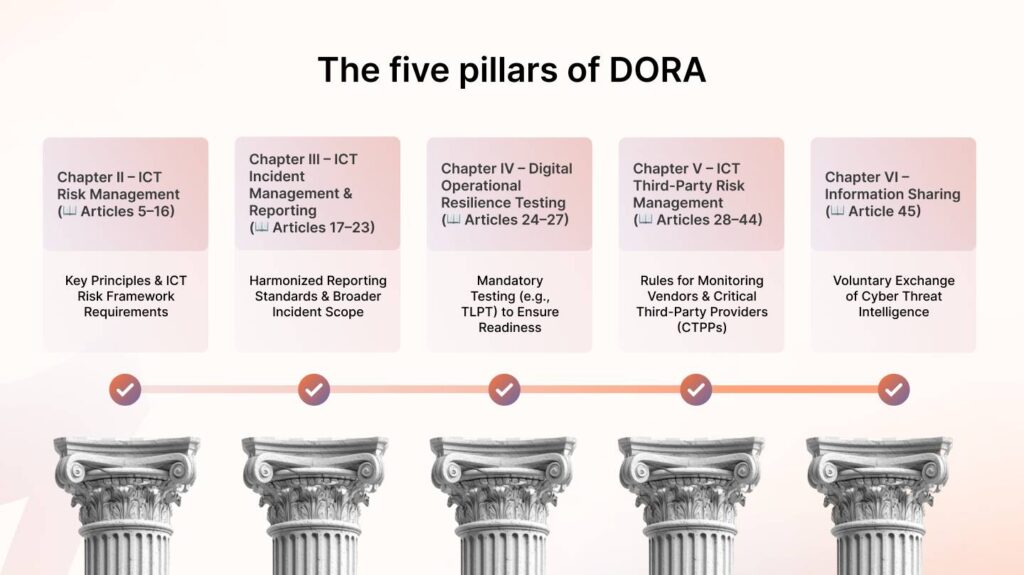

The five pillars of DORA

DORA is structured around five key pillars, each designed to strengthen financial institutions against cyber threats, IT disruptions, and third-party risks. But these pillars aren’t just separate requirements—they are interconnected, meaning a weak foundation in one area can affect compliance across the board.

With the European Supervisory Authorities (ESAs) releasing new technical standards in two batches (January 2024 and July 2024), financial institutions must adapt their compliance strategies to align with these evolving details.

ICT risk management

At the core of DORA is a robust Information and Communication Technology (ICT) risk management framework. This pillar is the backbone of the regulation, setting the stage for how financial firms identify, manage, and mitigate technology risks.

Here’s what it requires:

- Establish a structured ICT risk framework aligned with ISO 27001 and NIST standards.

- Define and classify critical business functions (CIFs)—a prerequisite for other pillars.

- Implement security controls (technical, organizational, and physical) to mitigate cyber risks.

- Develop a documented response and recovery strategy for cyber incidents and IT failures.

- Regularly test and refine risk management strategies based on real-world attack scenarios.

Incident reporting

Financial institutions are already required to report significant cybersecurity incidents, but DORA standardizes and expands this obligation, requiring firms to classify, document, and report disruptions in a structured format.

Here are the key compliance requirements:

- Classify major incidents using standardized templates.

- Report cybersecurity events and significant threats to regulators in a timely manner.

- Keep detailed incident logs for compliance audits and forensic analysis.

- Develop a post-incident strategy to learn from disruptions and prevent recurrence.

These standards are a far stricter version of previous frameworks like PSD2

Third-party risk management

Financial institutions are fully responsible for the resilience of their third-party service providers—whether cloud vendors, payment processors, or IT security firms. If a vendor goes down, you’re still accountable.

Compliance requirements include:

- Conduct due diligence before onboarding vendors to ensure they meet resilience standards.

- Continuously monitor vendor performance with periodic audits and risk reviews.

- Renegotiate contracts to include resilience obligations, including clear SLAs.

- Develop an exit strategy to ensure business continuity if a vendor fails.

Resilience testing

DORA requires you to prove resilience through rigorous stress testing. This pillar ensures that firms don’t just assume their systems will hold up under attack—they know they will.

Under resilience testing, financial institutions are required to:

- Perform regular penetration testing to find vulnerabilities before attackers do.

- Conduct stress tests and scenario-based simulations for cyber threats and system failures.

- Engage independent security testers for periodic evaluations.

- Implement continuous monitoring tools to detect weaknesses before they escalate.

Note: The RTS, or the Regulatory Technical Standard Threat-Led Penetration Testing (TLPT), has introduced mandatory penetration tests for financial institutions. This aligns with the TIBER-EU framework while introducing new mandates, such as allowing internal testers under certain conditions and making purple-team testing mandatory.

DORA allows Member States to designate a Single Public Authority (SPA) responsible for all TLPT-related tasks and responsibilities. However, Article 26(10) of DORA also gives Member States the flexibility to:

- Delegate some tasks to another authority while retaining primary oversight.

- Keep all TLPT-related responsibilities centralized under one competent authority.

Information and intelligence sharing

Cybercriminals share intelligence, evolve tactics, and exploit weaknesses in real-time. DORA mandates that financial institutions do the same, fostering industry-wide threat intelligence sharing to stay ahead of cyber threats.

Institutions need to:

- Develop secure mechanisms for sharing cybersecurity threat intelligence.

- Collaborate with industry peers to stay ahead of emerging threats.

- Use structured reporting formats to ensure consistency in intelligence sharing.

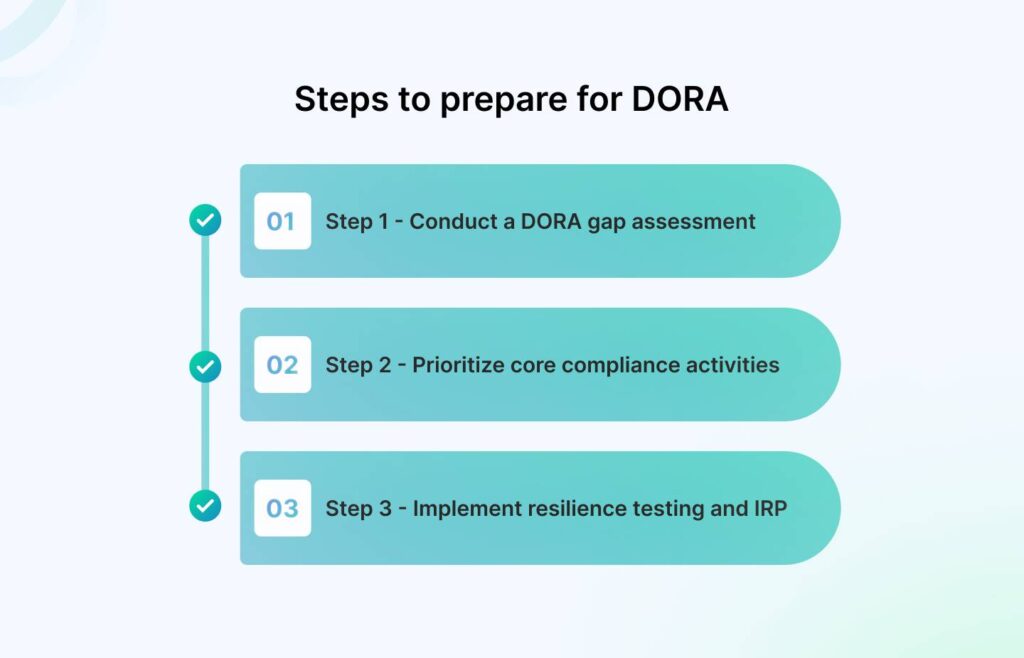

All this said and done, where should financial institutions begin?

How can organizations start preparing for DORA?

The complexity of DORA lies in its interconnected requirements—you can’t tackle third-party risk management without first mapping your ICT systems, and you can’t implement resilience testing without a strong incident response framework.

Step 1 – Conduct a DORA gap assessment

- Review existing policies, procedures, and security frameworks (e.g., ISO 27001, NIST CSF).

- Identify compliance gaps in ICT risk management, incident reporting, resilience testing, and third-party oversight.

- Engage with regulators early to clarify country-specific TLPT implementation.

Step 2 – Prioritize core compliance activities

- Critical ICT system mapping lays the groundwork for incident classification, resilience testing, and third-party risk assessments.

- Establish internal reporting workflows that align with DORA’s structured incident reporting requirements.

- Begin renegotiating vendor contracts to meet DORA’s third-party risk management standards.

Step 3 – Implement resilience testing and IRP

- Adopt continuous monitoring tools to detect and manage ICT risks proactively.

- Run cyber resilience simulations (penetration tests, stress tests) to validate business continuity under attack scenarios.

- Ensure third-party service providers are integrated into resilience testing frameworks

And lastly;

- Monitor updates from the European Supervisory Authorities (ESAs) as secondary legislation evolves.

- Leverage peer collaboration and industry intelligence-sharing to anticipate compliance roadblocks.

DORA doesn’t allow for a last-minute scramble—its requirements are prescriptive, enforceable, and require demonstrated resilience.

Implement DORA with Sprinto

Why is DORA needed?

If DORA didn’t exist, would financial institutions still prioritize resilience as they should? History suggests otherwise.

Failures that highlight the need for a stronger mandate:

- The ION trading outage of 2022 that crippled the derivatives market across Europe and the United States of America.

- TBS bank IT meltdown of 2018 that locked 2 million customers out of their bank accounts for weeks.

- Capital one data breach of 2019 led to the stealing of 106 million customer records.

With that, here’s what DORA aims to fix:

- Before DORA, each financial institution interpreted resilience differently. Now, there’s a unified, enforceable framework.

- Financial firms rely heavily on cloud providers, fintech vendors, and IT partners but had limited oversight over their security posture. DORA forces firms to take accountability for their entire supply chain.

- Many firms underreported cyber incidents or handled them inconsistently across jurisdictions. DORA standardizes incident classification, reporting, and response mechanisms.

- Simply having cybersecurity policies isn’t enough. Firms must now stress-test their systems and demonstrate their ability to withstand disruptions.

Under the Digital Operational Resilience Act (DORA), the essence lies in the five pillars that ensure financial entities maintain operational integrity and reliability. This involves directly or indirectly securing a comprehensive range of ICT capabilities through third-party services. These capabilities are critical for safeguarding network and information systems, thereby supporting the uninterrupted provision of financial services, especially during disruptions – Rachna Dutta. Infosecurity consultant, Sprinto.

Rachna Dutta, Infosecurity consultant, Sprinto

Great advice adds up. Get more from the brightest minds in GRC — join now

Will DORA affect your organization? If yes, how?

One of the most common questions we hear is: “Does DORA apply to us?” The short answer?

If your organization operates in the financial sector within the EU—or provides critical IT services to financial entities—then yes, DORA will impact you.

DORA has a broad scope, covering almost all regulated financial institutions and ICT third-party service providers that support them. The regulation doesn’t just target banks and investment firms—it extends to a wide ecosystem of financial and technology providers.

Who falls under DORA?

Financial entities

- Banks and credit institutions

- Insurance and reinsurance companies

- Investment firms

- Payment service providers (PSPs)

- Crypto-asset service providers (CASPs)

- Trading platforms and securities exchanges

- Central securities depositories (CSDs)

- Crowdfunding platforms

- Management companies of alternative investment funds (AIFMs)

- Financial market infrastructures (FMIs)

ICT Third-Party Providers

- Cloud computing providers

- Data centers and IT infrastructure providers

- Cybersecurity service providers

- Payment processors and financial software vendors

- Fintech companies supporting regulated financial institutions

The follow-up to this is usually, “But what if my organization is not directly involved/regulated?

Even if your firm isn’t a financial institution, you may still be impacted. If you provide IT services to DORA-regulated entities, expect:

- Increased compliance expectations from your financial clients.

- Contract renegotiations to align with DORA’s third-party risk management rules.

- Potential regulatory designation as a “Critical Third-Party Provider” (CTPP), subjecting your firm to direct oversight.

If DORA applies to your organization, compliance is legally enforceable.

DORA enforcement: what happens if organizations are non-compliant?

DORA will be enforced by National Competent Authorities (NCAs) in each EU Member State, meaning regulatory oversight will vary across jurisdictions. However, the European Supervisory Authorities (ESAs) will have a direct role for specific areas like third-party risk management, particularly in overseeing Critical Third-Party Providers (CTPPs).

Each country can designate a Single Public Authority (SPA) to oversee resilience testing, and some may delegate specific tasks to multiple agencies, creating jurisdictional nuances that firms operating across multiple EU states will need to track.

What are the penalties for non-compliance?

Regulatory authorities will have the power to:

- Significant fines for failing to comply with DORA’s requirements. The Member States will determine the exact amounts.

- If an organization’s resilience framework is inadequate, regulators may limit or suspend certain activities until compliance is achieved.

- Firms may be required to remediate security weaknesses, strengthen controls, or undergo additional stress testing to demonstrate compliance.

- Severe violations could result in public disclosure of enforcement actions, which could damage reputation and cause a loss of client trust.

Current status of DORA

Financial institutions and ICT service providers have until January 17, 2025, to fully comply with DORA (Digital Operational Resilience Act). This marks the end of the two-year implementation period when DORA entered into force on January 16, 2023.

From January 17, 2025, regulators will begin actively monitoring compliance, and enforcement actions could follow for organizations that fail to meet the required standards. Some obligations, such as critical third-party oversight and advanced penetration testing (TLPT), will phase in gradually. However, firms must still have their foundational resilience measures before the deadline.

If you’re looking for a DORA partner, look no further.

How can Sprinto help with DORA?

Sprinto simplifies DORA compliance by mapping the regulation’s requirements to globally recognized frameworks like the Secure Controls Framework (SCF), ISO 27001, and SOC 2—reducing manual effort and ensuring continuous compliance.

- In collaboration with trusted implementation partners, Sprinto helps organizations identify compliance gaps by assessing existing security policies, risk management frameworks, and resilience measures against DORA’s five core pillars.

- Sprinto’s ISO 27005-aligned risk register allows organizations to efficiently identify, assess, and mitigate ICT risks.

- It helps organizations implement DORA’s structured incident reporting framework, ensuring rapid classification, response, and disclosure of ICT incidents.

- Sprinto helps organizations implement DORA’s structured incident reporting framework, ensuring rapid classification, response, and disclosure of ICT incidents.

Frequently Asked Questions

What qualifies as a significant ICT-related incident under DORA?

A major ICT-related incident is any disruption significantly impacting the financial services sector, causing operational failure, data breaches, or service downtime. Firms must classify incidents based on severity, report them to regulators within the required timeframe, and maintain detailed logs for forensic analysis.

How does DORA help financial institutions manage operational risk?

DORA mandates a structured operational risk management framework, requiring firms to identify, assess, and mitigate ICT threats that could disrupt financial operations. This includes cyber resilience measures, real-time risk monitoring, and regular resilience testing to prevent systemic failures.

How does DORA affect financial services firms that rely on cloud service providers?

DORA places direct accountability on financial institutions for the resilience of their cloud service providers and other third-party vendors. Firms must assess third-party risks, renegotiate contracts to include DORA-compliant security clauses, and ensure that vendors participate in resilience testing and regulatory oversight.

What are critical assets under DORA, and why do they matter?

Critical assets include core ICT systems, data repositories, and third-party services essential for financial operations. DORA requires firms to map dependencies, implement security controls, and stress-test these assets to ensure continuity in the face of cyber threats or technical failures.

What is the role of operational resilience testing in DORA compliance?

Operational resilience testing ensures that financial entities can withstand disruptions by conducting penetration, stress, and threat-led penetration testing (TLPT) every three years for high-risk firms. These tests help identify vulnerabilities, improve incident response, and validate business continuity plans.

Author

Heer Chheda

Heer is a content marketer at Sprinto. With a degree in Media, she has a knack for crafting words that drive results. When she’s not breaking down complex cyber topics, you can find her swimming or relaxing by cooking a meal. A fan of geopolitics, she’s always ready for a debate.Go beyond the surface and uncover the governance, risk, and compliance insights that actually matter.

Win digital goodies for boardroom success

Explore more

research & insights curated to help you earn a seat at the table.